Smart Budgeting……Managing money can feel overwhelming when you’re just getting started. Between rent, groceries, transportation, insurance, and entertainment, expenses in the United States can quickly add up. The good news is that budgeting doesn’t have to be complicated. With the right approach, anyone can create a simple system to control spending, save money, and build financial stability.

This beginner’s guide will walk you through the basics of budgeting in the U.S. in 2026 — from understanding income and expenses to choosing tools that make managing money easier.

Why Budgeting Matters in 2026

The cost of living in the United States continues to change due to inflation, housing demand, and economic trends tracked by institutions like the Federal Reserve. Because everyday expenses fluctuate, budgeting is no longer optional — it’s essential.

A good budget helps you:

- Avoid unnecessary debt

- Reduce financial stress

- Build emergency savings

- Plan for long-term goals

- Spend money with confidence

Instead of wondering where your money goes each month, a budget gives you clarity and control.

1: Understand Your Monthly Income

Before creating a budget, you need to know exactly how much money you bring home each month after taxes. This is called net income, or “take-home pay.”

Your income may include:

- Full-time or part-time salary

- Freelance or gig work income

- Government benefits

- Investment income

- Side hustle earnings

If your income changes monthly, calculate an average from the last three to six months. This gives you a realistic baseline for budgeting.

Knowing your true income prevents overspending and helps you plan responsibly.

2: Track Your Monthly Expenses

The next step is understanding where your money goes. Many Americans underestimate their spending, especially on small daily purchases.

Common expense categories include:

Fixed expenses

- Rent or mortgage

- Car payment

- Insurance

- Phone bills

- Internet service

These costs usually stay the same every month, making them easier to plan for.

Variable expenses

- Groceries

- Gas

- Dining out

- Shopping

- Entertainment

These change monthly and often provide the biggest opportunity to save money.

Tracking expenses for at least one month gives you a clear financial picture. You can do this using a notebook, spreadsheet, or budgeting app.

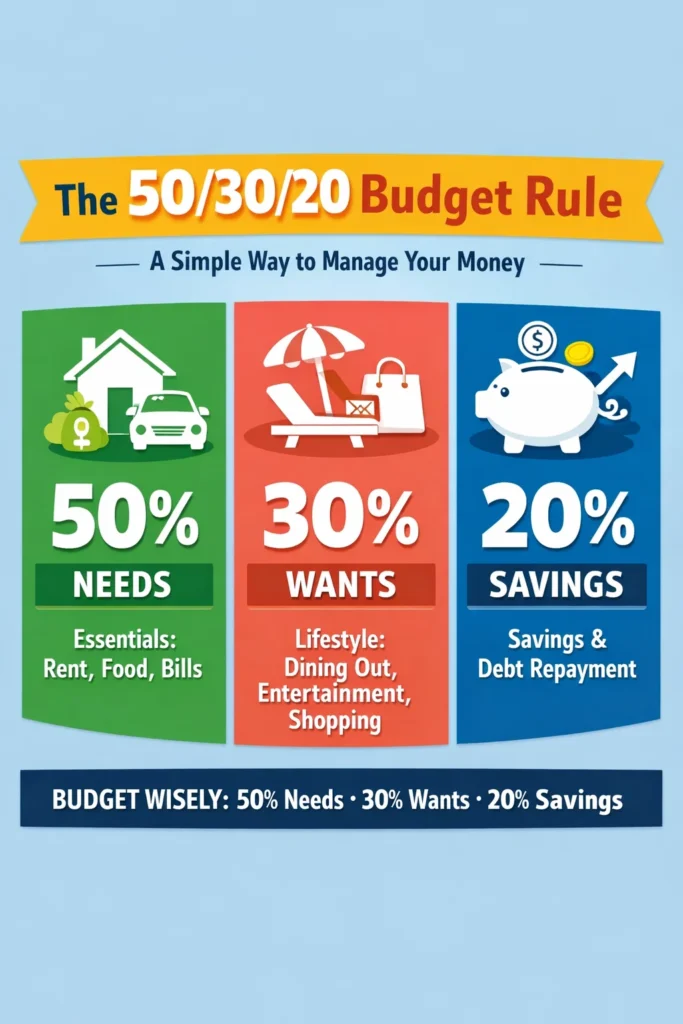

3: Use the 50/30/20 Budget Rule

One of the easiest budgeting methods for beginners is the 50/30/20 rule. It divides your income into three categories.

- 50% for needs

This includes housing, utilities, groceries, transportation, insurance, and minimum loan payments. These are essential living costs you cannot avoid. - 30% for wants

Dining out, streaming subscriptions, hobbies, travel, and entertainment fall into this category. These expenses improve quality of life but aren’t necessary. - 20% for savings and debt repayment

Emergency funds, retirement contributions, and extra debt payments belong here. This category helps secure your financial future.

This simple structure makes budgeting less intimidating and easier to maintain long term.

4: Build an Emergency Fund

Unexpected expenses happen to everyone — medical bills, car repairs, or job loss. That’s why an emergency fund is a key part of budgeting.

Financial experts in the U.S. typically recommend saving three to six months of essential expenses.

Start small if needed:

- Save $500 first

- Then build toward $1,000

- Eventually grow to several months of expenses

Even small savings create financial security and reduce reliance on credit cards or loans.

Consistency matters more than the amount you save at the beginning.

5: Choose a Budgeting Method That Works

There’s no single “perfect” budget system. The best method is the one you’ll actually use.

Here are a few beginner-friendly options:

- Zero-based budgeting

Every dollar of income gets assigned a purpose — spending, saving, or investing. This method gives maximum control over money and reduces wasteful spending. - Envelope budgeting

Money is divided into spending categories. Once a category runs out, you stop spending in that area. This method builds strong discipline and awareness. - Digital budgeting apps

Apps automatically track spending and categorize transactions. Popular tools include Mint and YNAB. These tools simplify budgeting for beginners who prefer automation.

The key is consistency, not complexity.

6: Reduce Common Monthly Expenses

Budgeting becomes easier when you lower unnecessary spending. Many Americans find savings in everyday expenses once they start reviewing them closely.

Look for opportunities like:

- Canceling unused subscriptions

- Cooking at home more often

- Comparing insurance providers

- Using public transportation occasionally

- Buying generic brands at grocery stores

These small changes can save hundreds of dollars per month without dramatically changing your lifestyle.

Budgeting isn’t about restriction — it’s about smarter spending.

7: Plan for Taxes and Retirement

In the U.S., taxes and retirement savings are important parts of financial planning.

Understanding basic tax responsibilities through the Internal Revenue Service helps you avoid surprises during tax season.

For retirement, common savings options include:

- Employer-sponsored 401(k) plans

- Individual Retirement Accounts (IRAs)

- Employer matching contributions

- Automatic payroll deductions

Starting retirement savings early allows compound growth to work in your favor. Even small monthly contributions can grow significantly over time.

Future planning is one of the biggest benefits of budgeting.

8: Review and Adjust Your Budget Monthly

A budget is not something you create once and forget. Your income, expenses, and goals will change over time.

Review your budget every month to:

- Adjust spending categories

- Track savings progress

- Identify problem areas

- Set new financial goals

Monthly reviews help you stay accountable and confident in your financial decisions.

Budgeting is a habit, not a one-time task.

Common Budgeting Mistakes to Avoid

Beginners often struggle with budgeting at first. That’s completely normal. Avoiding these mistakes can make the process smoother.

- Being too strict

Unrealistic budgets often fail quickly. Allow room for fun and flexibility so your budget feels sustainable. - Not tracking small purchases

Coffee, snacks, and online purchases add up faster than expected. Tracking everything creates awareness and control. - Ignoring irregular expenses

Car maintenance, holiday gifts, and medical costs don’t happen monthly but still need planning. - Giving up too soon

Budgeting takes time to become comfortable. Most people need two or three months to build the habit.

Progress matters more than perfection.

Conclusion

Budgeting in the United States in 2026 doesn’t require complicated financial knowledge or expensive tools. It simply requires awareness, planning, and consistency.

When you understand your income, track expenses, follow a simple budgeting method, and build savings gradually, you create a strong financial foundation.

Remember: budgeting isn’t about limiting your life — it’s about giving your money direction and purpose.

The earlier you start, the easier financial stability becomes.

Why is budgeting important for living comfortably in the USA?

Budgeting helps you manage income, control spending, and save for future goals. With the high cost of housing, healthcare, and transportation in the USA, a clear budget helps maintain financial stability and avoid unnecessary debt.

How much should I save each month?

A common rule is to save at least 20% of your monthly income if possible. Even small, consistent savings can build financial security over time and help cover emergencies.

What is the 50/30/20 budgeting rule?

The 50/30/20 rule suggests spending 50% of income on needs, 30% on wants, and saving 20%. This simple method helps balance daily expenses while building savings.

What are the biggest expenses people should plan for in the USA?

Housing, transportation, healthcare, groceries, and insurance are typically the largest monthly expenses. Planning for these costs first makes budgeting easier and more realistic.

How can beginners start budgeting easily?

Start by tracking your income and expenses, setting spending limits, and reviewing your budget monthly. Using simple budgeting apps or spreadsheets can make the process easier and more consistent.