Paying for college or university can be expensive, and many students need financial help to cover tuition, books, and living costs. To support students in pursuing higher education, the U.S. government offers financial assistance through the Federal Student Loan Program. This program helps students pay for their education by providing government-backed loans with flexible terms.

A federal student loan is money borrowed from the U.S. government to help pay for college expenses. Compared to private education loans or private school loans, federal loans usually offer lower interest rates and more flexible repayment options. In addition, many borrowers may qualify for benefits such as student loan forgiveness or income-driven repayment plans, making federal loans a popular choice among students.

Students can apply for federal student aid through the official website StudentAid.gov, which is managed by Federal Student Aid. By completing the application, eligible students may receive financial support through grants, work-study programs, and federal loans.

Overall, the federal student loan program plays an important role in making higher education more accessible by helping millions of students finance their college education each year.

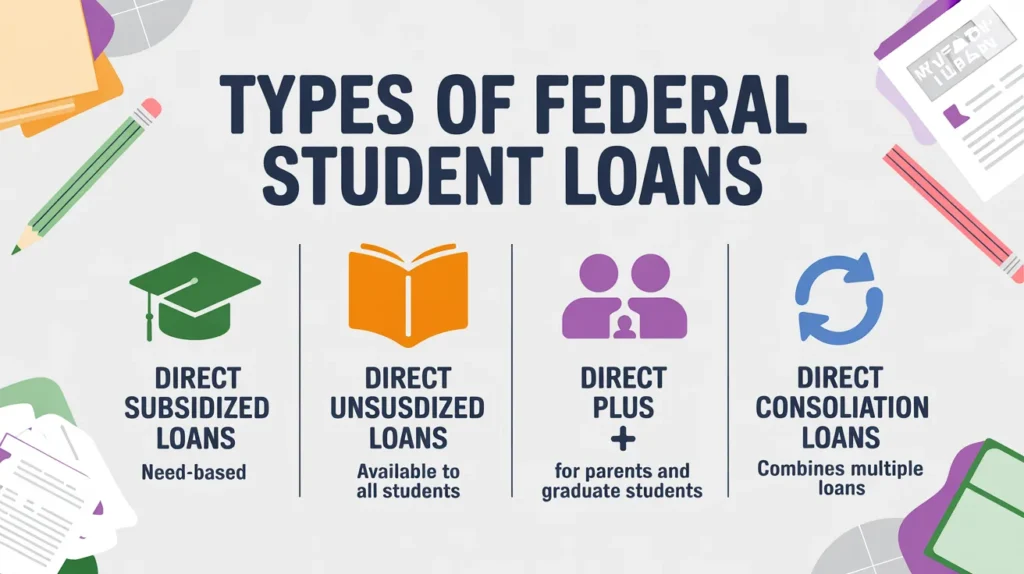

Types of Federal Student Loans

The Federal Student Loan Program offers several types of loans to help students and parents pay for higher education. These federal student loans are designed with different benefits and eligibility requirements so that students from various financial backgrounds can receive support. Below are the main types of federal student loan options available through Federal Student Aid.

1. Direct Subsidized Loans

Direct Subsidized Loans are available to undergraduate students who demonstrate financial need. The key advantage of this federal student loan is that the U.S. government pays the interest while the student is in school at least half-time, during the grace period, and during certain deferment periods. Because of this benefit, Direct Subsidized Loans are often considered one of the most affordable student loans for eligible students.

2. Direct Unsubsidized Loans

Direct Unsubsidized Loans are available to undergraduate, graduate, and professional students, and they do not require proof of financial need. Unlike subsidized loans, the borrower is responsible for paying all the interest that accumulates from the time the loan is disbursed. However, these loans still offer flexible repayment options compared to many private education loans.

3. Direct PLUS Loans

Direct PLUS Loans are designed for graduate students or parents of dependent undergraduate students. These loans help cover educational costs that are not fully covered by other financial aid. While they typically have higher interest rates than other federal student loans, they still provide benefits such as access to federal repayment plans and potential loan forgiveness options.

4. Direct Consolidation Loans

A Direct Consolidation Loan allows borrowers to combine multiple federal student loans into a single loan with one monthly payment. This can make repayment easier to manage and may also allow borrowers to qualify for certain repayment plans or student loan forgiveness programs.

Students who want to apply for any of these federal student loans must complete the application process through the official website StudentAid.gov, which is part of the federal student aid system. Understanding the different types of loans can help students choose the option that best fits their educational and financial needs.

Benefits of Federal Student Loans

A federal student loan is one of the most reliable ways for students to finance their college education. These loans are provided through the Federal Student Loan Program, which is managed by Federal Student Aid. Compared to many private education loans or private school loans, federal loans offer several important advantages that make them a preferred option for students.

1. Lower Interest Rates

One of the biggest benefits of federal student loans is that they usually have lower and fixed interest rates compared to most private education loans. This helps students manage their loan payments more easily after graduation.

2. Flexible Repayment Options

Federal loans offer multiple repayment plans designed to make repayment more manageable. Borrowers can choose income-driven repayment plans that adjust monthly payments based on their income and family size.

3. Student Loan Forgiveness Programs

Many borrowers may qualify for student loan forgiveness programs after meeting specific requirements. For example, people working in public service or certain nonprofit jobs may be eligible for loan forgiveness, which can reduce or eliminate the remaining loan balance.

4. Grace Period After Graduation

Most federal student loans provide a grace period of about six months after graduation before repayment begins. This gives graduates time to find a job and stabilize their finances before making payments.

5. No Credit Check for Most Loans

Unlike many private school loans, most federal loans do not require a credit check or a co-signer. This makes it easier for students to qualify for financial assistance.

6. Access Through StudentAid.gov

Students can easily apply for federal student aid, including student loans, through the official website StudentAid.gov. This platform provides reliable information and guidance for students seeking financial support for their education.

Because of these benefits, federal loans remain one of the most accessible and student-friendly options for financing higher education in the United States.

Eligibility and What You Need for Federal Student Loans

To receive a federal student loan, students must meet certain eligibility requirements set by the Federal Student Aid under the Federal Student Loan Program. These requirements ensure that financial aid is provided to students who qualify for federal student aid and need support for their education.

Basic Eligibility Requirements

To qualify for federal student loans, students generally must:

- Be a U.S. citizen or an eligible non-citizen

- Have a valid Social Security number

- Possess a high school diploma, GED, or equivalent qualification

- Be enrolled or accepted in an eligible college or university program

- Bank Statements or Financial Records Provides information about assets and financial status.

- Maintain satisfactory academic progress in school

- Not be in default on any existing federal student loans

Meeting these requirements allows students to apply for financial assistance through the federal aid system.

What You Need to Apply

To apply for a federal student loan, students must complete the financial aid application through StudentAid.gov. During the application process, you will typically need the following information:

- Your Social Security number

- Tax returns or income information (for you or your parents, if required)

- School information for the college you plan to attend

- Records of bank accounts or investments, if applicable

This information helps determine your eligibility for federal student aid, including grants, work-study programs, and federal student loans.

Federal Loan Program Limits

The Federal Student Loan Program sets borrowing limits to ensure students do not take on excessive debt. These limits apply mainly to Direct Subsidized and Direct Unsubsidized loans provided through Federal Student Aid.

Annual Federal Student Loan Limits

| Student Level | Maximum Annual Loan Limit |

| First-Year Undergraduate | $5,500 |

| Second-Year Undergraduate | $6,500 |

| Third-Year and Beyond Undergraduate | $7,500 |

| Graduate or Professional Students | $20,500 |

Total (Aggregate) Federal Student Loan Limits

| Student Type | Total Loan Limit |

| Dependent Undergraduate Students | $31,000 |

| Independent Undergraduate Students | $57,500 |

| Graduate or Professional Students | $138,500 |

These limits apply to most federal student loans under the federal student aid system. Students can check the latest details and apply for financial aid through StudentAid.gov.

Federal Student Loan Repayment Options

| Repayment Plan | Key Features |

| Standard Repayment Plan | Fixed monthly payments for up to 10 years. Usually results in the lowest total interest paid. |

| Graduated Repayment Plan | Payments start low and gradually increase every two years, typically over 10 years. |

| Extended Repayment Plan | Allows smaller monthly payments by extending the repayment period up to 25 years. |

| Income-Driven Repayment Plans | Monthly payments are based on income and family size, making payments more affordable. |

Borrowers with a federal student loan have several flexible repayment plans designed to make paying back federal student loans more manageable. These plans are offered through Federal Student Aid under the Federal Student Loan Program.

How to Apply for a Federal Student Loan (Step-by-Step Guide)

Applying for a federal student loan is a simple process when you follow the correct steps. The application is handled through the Federal Student Loan Program and managed by Federal Student Aid.

Follow these steps to apply for federal loans:

- Create an FSA ID

Visit StudentAid.gov and create your FSA ID. This account allows you to access and manage your federal student aid application. - Complete the FAFSA Application

Fill out the Free Application for Federal Student Aid (FAFSA) on StudentAid.gov. This form determines your eligibility for federal student aid, including grants, work-study programs, and student loans. - Submit Required Financial Information

Provide necessary documents such as your Social Security number, tax returns, and income details to verify your financial situation. - Review Your Financial Aid Offer

After processing your FAFSA, your chosen college or university will send a financial aid offer that may include federal student loans. - Accept the Loan Amount

Decide how much of the offered federal loan you want to accept. You are not required to accept the full amount. - Complete Entrance Counseling

First-time borrowers must complete entrance counseling to understand their responsibilities before receiving student loans. - Sign the Master Promissory Note (MPN)

This is a legal agreement confirming that you will repay the federal loan and any applicable interest. - Receive Loan Funds

Once approved, the loan funds are sent directly to your school to cover tuition and other education expenses.

Federal Education Loan Repayment Options

Borrowers with a federal loan have several repayment options designed to make paying back student loans easier and more manageable. These plans are offered through Federal Student Aid as part of the Federal Student Loan Program.

- Standard Repayment Plan

Fixed monthly payments over 10 years. This plan usually results in the lowest total interest paid. - Graduated Repayment Plan

Payments start lower and gradually increase every two years, usually within a 10-year repayment period. - Extended Repayment Plan

Allows smaller monthly payments by extending the repayment term up to 25 years. - Income-Driven Repayment Plans

Monthly payments are based on income and family size, making repayment more affordable. Some borrowers may also qualify for student loan forgiveness after a certain number of qualifying payments.

Borrowers can review and manage their loans and repayment plans through the official website StudentAid.gov.

What is the difference between federal student loans and private student loans?

Federal student loans are funded by the U.S. government and usually offer more flexible repayment options, lower interest rates, and borrower protections such as income-driven repayment plans and potential loan forgiveness programs. Private student loans are provided by banks, credit unions, or private lenders. They often require a credit check or co-signer and typically offer fewer repayment protections compared to federal loans.

When do I have to start repaying my federal student loan?

Most federal student loans have a grace period of about six months after you graduate, leave school, or drop below half-time enrollment. During this time you are not required to make payments. After the grace period ends, regular monthly payments begin unless you enroll in a different repayment plan or qualify for deferment or forbearance.

Can federal student loans be forgiven?

Yes, certain federal student loans may qualify for forgiveness under specific programs. Examples include Public Service Loan Forgiveness (PSLF) for people working in government or nonprofit organizations and income-driven repayment forgiveness after a set number of years of qualifying payments. Eligibility depends on factors such as employment, repayment plan, and payment history.

What happens if I cannot repay my federal student loan?

If you are struggling to make payments, federal student loans offer several options. You may qualify for income-driven repayment plans that lower monthly payments based on your income. You can also apply for deferment or forbearance to temporarily pause payments during financial hardship. Ignoring the loan completely can lead to default, which may damage your credit and lead to collection actions.

Can international students apply for federal student loans?

In most cases, federal student loans are only available to U.S. citizens or eligible non-citizens such as permanent residents. International students usually do not qualify for federal student aid. However, they may be able to apply for private student loans through lenders, often with a creditworthy U.S. co-signer.

Are federal student loan interest rates fixed or variable?

Federal student loan interest rates are fixed, meaning the rate remains the same for the entire life of the loan. The rate is set each year by the U.S. government for new loans issued during that academic year. This provides predictable monthly payments compared to many private loans that may have variable interest rates.

Is there a limit to how much I can borrow in federal student loans?

Yes, federal student loans have annual and lifetime borrowing limits. The amount you can borrow depends on your year in school, dependency status, and the type of loan program. For example, undergraduate students have lower limits compared to graduate students. These limits are designed to help prevent students from taking on excessive debt.